What does the FSRA consider to be a Digital Security?

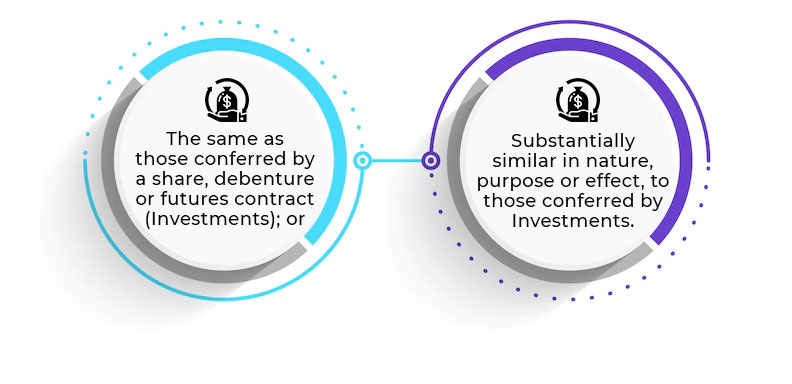

In addition, a Digital Security is defined as a token that confers

rights and obligations that are:

In effect, a Digital Security is a token that behaves as a

security (equity, debenture, convertible, future, option etc.) and

is hence considered by the FSRA as a Security and a Specified

Investment.

What is a Security?

The FSRA has a list of instruments that they consider a security.

In general, a transaction is considered a security if a) There is

an investment of money, b) There is an expectation of profit, c)

The investment of money is in a common enterprise and d) Any

profit comes from the efforts of a promoter or third party. This

is also commonly known as the Howey Test.

How are Utility Tokens classified under the ADGM Virtual Assets

Framework?

Utility Tokens, i.e. tokens that can be redeemed for access to a

specified product or service are treated as commodities and hence

not deemed Specified Investments. Trading and transactions in

Utility Tokens are not regulated, unless they are caught as

Accepted Virtual Assets.

What Are Accepted Virtual Assets in the ADGM?

The FSRA would require third-party verification to demonstrate

that the Virtual Asset meets security requirements to be deemed an

accepted Virtual Asset.

The considerations would include:

Market capitalization and sufficiency of client demand, proportion

in free float and the control mechanisms to manage volatility.

Security – the ability of the Virtual Asset to respond and adapt

to vulnerabilities Origin and destination of the virtual asset,

ability to identify counterparties in transactions and monitoring

of on-chain transactions.

Number of exchanges where the Virtual Asset is listed and the

depth of regulation of such exchanges.

Type of DLT used

Depth of innovation of the Virtual Asset and practicaility of

application.

Virtual Asset Service Provider activities in the ADGM

The VASP activities that are covered by the ADGM Virtual Assets

Framework include:

The ADGM has an existing framework for the authorization and

regulation of Exchanges, Alternative Trading Systems and Clearing

houses. Under the regulation for conventional securities,

exchanges are licensed as Authorised Market Institutions (AMI),

and MTFs and OTFs are licensed as Alternative Trading Systems.

Accordingly, the FSRA permits such institutions to perform the

same activities for Virtual Assets as well. However, privacy

tokens and anonymous trading will not be allowed.

There are additional requirements applicable to such facilities,

mainly comprising KYC and technology-related compliances.

Additional IT-related requirements

The FSRA would be interested in reviewing the criteria for market

participants who access and update records on the platform,

network security and ongoing compliances. They would also review

the IT design of the DLT implementation adopted by the VASP that

trades virtual assets, and whether it is able to address how the

rights and obligations relating to the tokens are properly

discharged.

Technology governance mechanisms would also be reviewed, including

IT architecture, storage and transmission of data, procedures to

address soft and hard forks, cyber-security measures,

decision-making protocols and interfaces with providers of digital

wallets.

A comprehensive IT audit, conducted by an independent third-party

IT expert would be required to be submitted to the FSRA annually.